Stripe Closed My Account with Money in It: A Full Recovery Guide for Merchants

Wed May 06 2026

You log into your dashboard, and the balance is frozen. A standard automated email has arrived: your Stripe terminated account notice. No specific reason or timeline, and the processing has stopped.

If this has happened to you, you're not alone. This guide covers exactly what happens when Stripe closes your account with money in it, your realistic options for recovery, and how to build infrastructure that doesn't leave your revenue hostage to a single processor's decision.

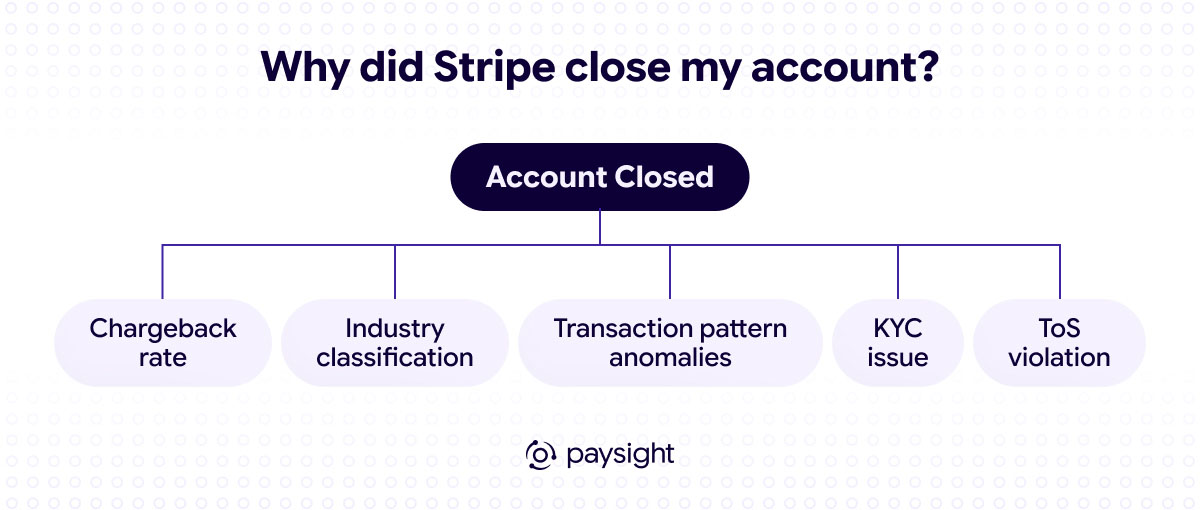

Why Stripe Closes Accounts?

Stripe is an aggregated payment processor, meaning all merchants process payments through its master merchant account. This gives Stripe broad power to terminate accounts at its sole discretion, and when you agreed to their Services Agreement, you accepted that.

The triggers that lead to closure fall into several consistent categories:

- High chargeback rates. Card networks set a general benchmark of 1% chargeback ratio. Exceed it or spike sharply even once, and Stripe's risk engine flags the account.

- Industry classification. Stripe maintains a list of prohibited and restricted business categories. Supplements, subscriptions, coaching, digital downloads, crypto, and travel face tighter scrutiny. If your business model evolved after signup, you may get shut down retroactively.

- Transaction pattern anomalies. Sudden volume spikes, high-value transactions, or processing patterns inconsistent with your stated business model trigger automated flags via Stripe's Radar system.

- KYC mismatches. Stripe approves accounts fast. As volume grows, they run enhanced due diligence. If documents don't match or the business model has shifted, the account gets suspended or closed.

- Terms of service violations. Unclear product descriptions, undisclosed business lines, or misrepresentation of your MCC all qualify.

The critical thing to understand: Stripe rarely explains which of these applies to you. The notification email is standardized, the support is limited, and reversals are rare.

What Actually Happens to Your Money

When Stripe closes your account with money in it, the funds are almost certainly not gone. They're held.

Stripe imposes a reserve on your balance to cover chargebacks, refunds, or disputes that cardholders can still raise after your account stops processing. Card networks give buyers dispute windows of 60 to 120 days from the transaction date, sometimes longer.

How long does Stripe hold your money?

- Clean account, no open disputes — closer to 90 days

- Elevated chargebacks or flagged activity — up to 180 days

- Active fraud investigation — potentially longer, with no fixed timeline

During the hold, you can still log into your dashboard to view transactions and monitor disputes, but you can't initiate payouts or new transactions. Check it regularly: Stripe can release funds gradually before the hold ends, so there's no point waiting for a lump-sum payout.

Once the hold period ends, Stripe transfers whatever remains to your linked bank account, after deducting chargebacks, refunds, and fees. Keep that account open and active until every payment has cleared, as if Stripe attempts a transfer to a closed account, the payout fails, and the delay restarts.

One scenario that catches merchants off guard: if your balance doesn't cover incoming chargebacks, Stripe can debit your linked bank account for the shortfall. If that debit fails, it can escalate to collections.

The bottom line: your money isn't confiscated, but it's not fully yours yet. Stripe froze your funds to manage liability, so plan your cash flow around that window.

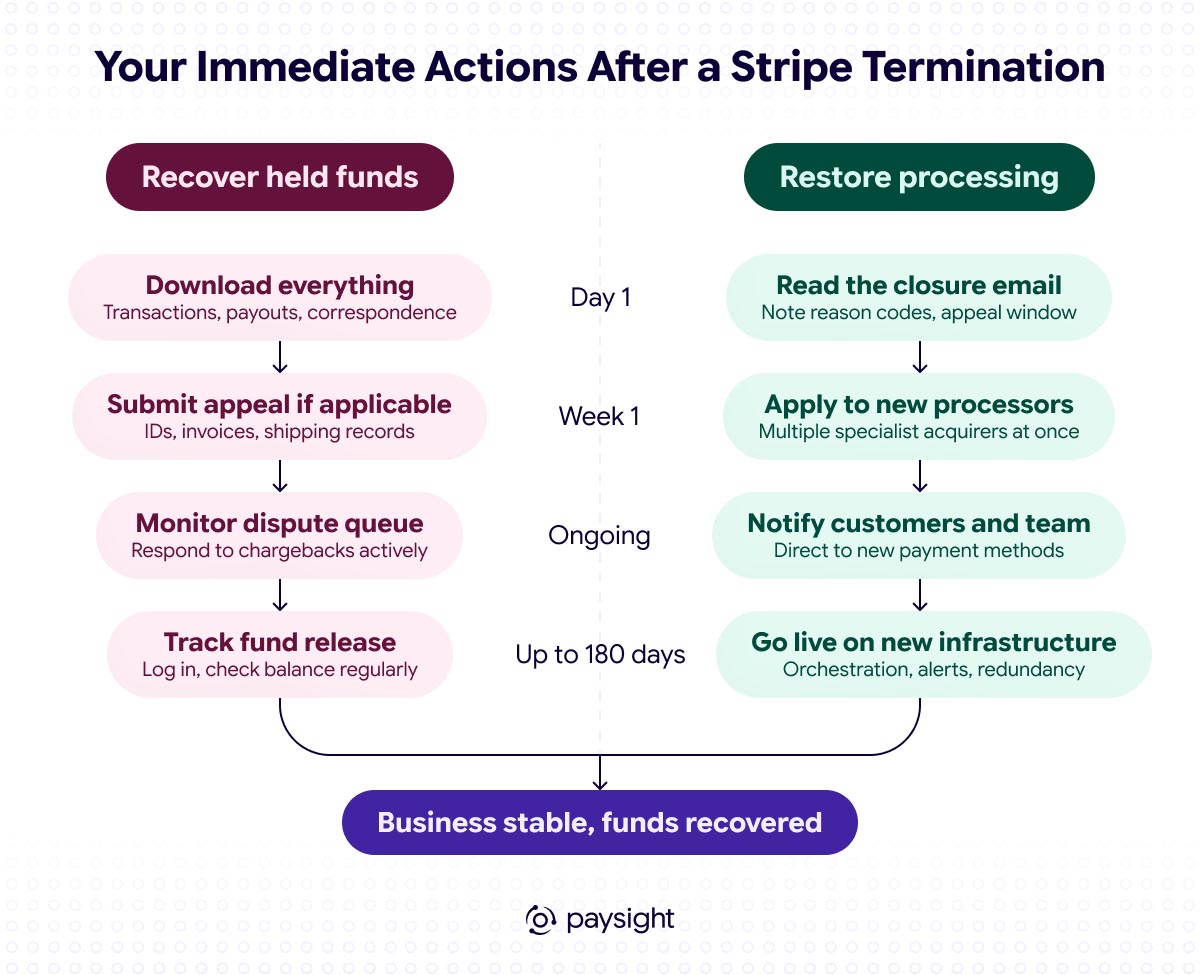

Your Immediate Actions After a Stripe Termination

When the closure notice lands, the sequence in which you act matters. These two problems — recovering held funds and restoring payment processing — need to be handled as parallel tracks, not one problem.

1. Document Everything Before Access Changes

Log in to your Stripe dashboard immediately. Screenshot or download your full transaction history, payout records, dispute history, and any correspondence from Stripe. If your dashboard access is restricted, save whatever you can from the closure email itself. This documentation is critical for two reasons: potential appeals and applications with future processors who will ask about your processing history.

2. Review the Closure Notification Carefully

The email, however vague it may seem, can contain a specific reason code or reference to a policy violation. Note the exact language. If Stripe's email invites you to provide additional information or documents to address the issue, respond promptly. Replying within the first week gives you the best chance of any review being reconsidered. Provide identity documents, invoices, shipping records, or compliance evidence as applicable.

3. Contact Stripe Support and Create a Paper Trail

Submit a formal inquiry through Stripe's support portal. Ask for clarification on the reason for closure and the timeline for the fund release. Document every interaction: date, time, and the response received. If you plan to escalate or if the hold extends beyond 180 days, this correspondence record becomes important.

If you believe the closure was in error and funds are not released after 180 days, that's the point at which legal counsel becomes relevant. Under the terms of their agreement and applicable financial law, Stripe cannot hold funds indefinitely.

4. Monitor Your Dispute Queue

During the hold period, log in regularly and track your dispute activity. Each chargeback that's resolved against you reduces your eventual payout. You still have the right to respond to disputes that come in during the hold, so fight for it. A well-documented response to a chargeback can directly affect the amount you recover.

5. Notify Customers and Operational Teams

Your team needs to know that processing is interrupted. But if you run subscriptions, this step is urgent on a different level: all recurring charges stop the moment your account is disabled. Stripe does not migrate subscriptions automatically. You need to either export customer payment tokens or ask customers to re-enter their payment details with a new processor. And you need to do it fast, before the next billing cycle triggers failed charges and disputes. The faster you communicate, the fewer disputes arise from customers who don't know why their payment was declined.

Restoring Payment Acceptance in the Right Way

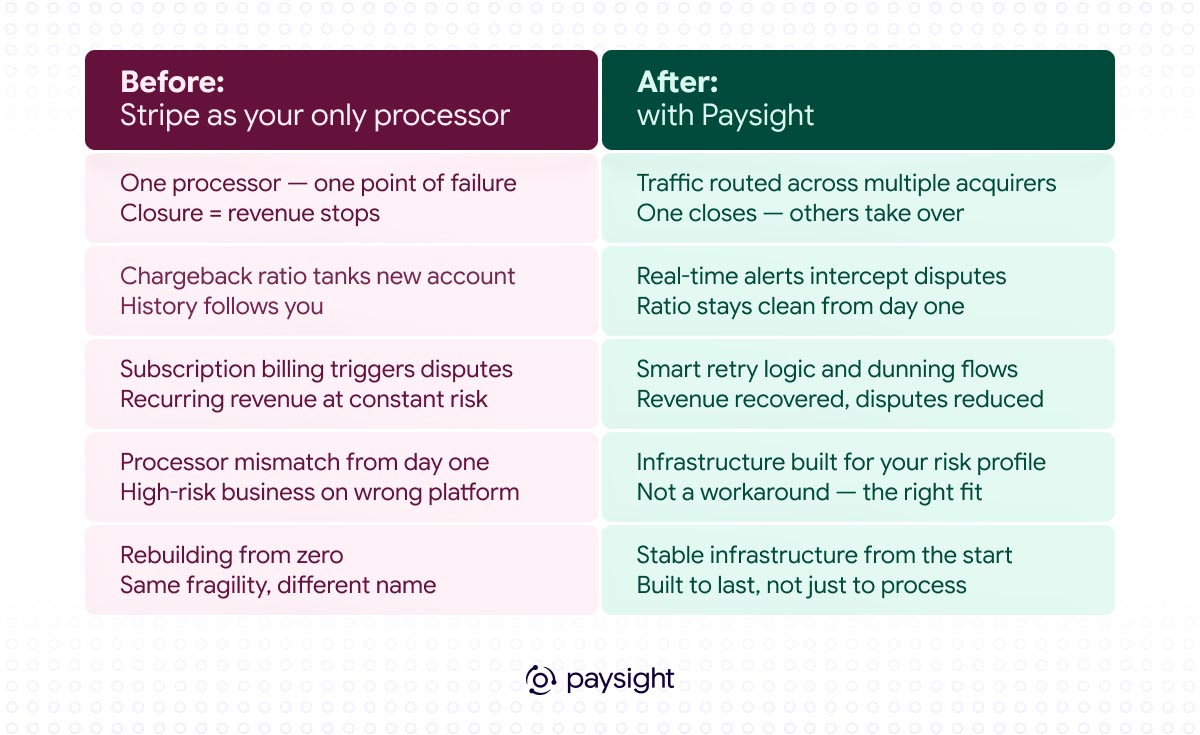

When merchants search for what to do after Stripe's closure, they can land on the same answer: sign up for another aggregator, like PayPal, Square, or Shopify Payments. The problem is that the same risk profile that got you shut down on Stripe will get you shut down there, too. And often even faster, because your account now carries a termination on record.

The right move depends on why you were closed.

If you're in a high-risk vertical

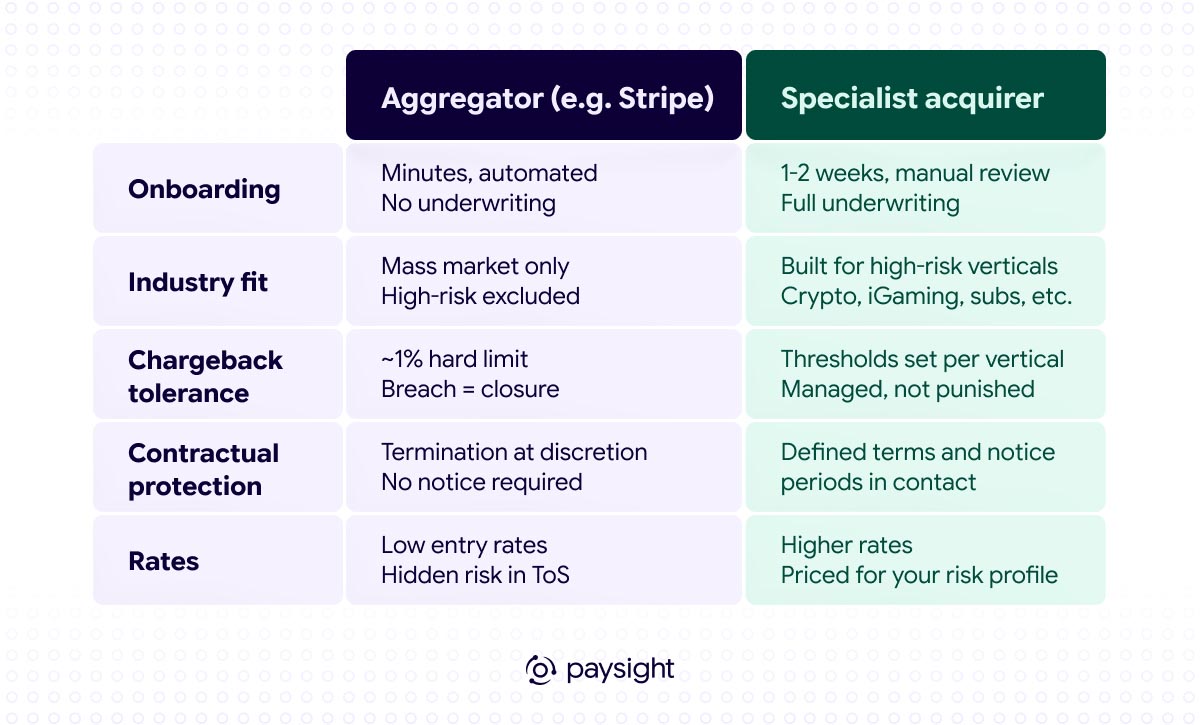

Supplements, subscriptions, crypto, iGaming, digital content, coaching, financial services… Are you in the list? Stripe was never the right fit for your business. You need a dedicated high-risk merchant account with a specialist acquirer who actually underwrites your category. Expect onboarding that takes one to two weeks, proper documentation, and higher rates. But in return, you get a processor built for your business model, appropriate chargeback thresholds, and contractual protections that aggregators don't offer. Apply to more than one simultaneously. Approval isn't guaranteed, and time matters.

If you process across multiple geographies or payment methods

A single new acquirer still leaves you exposed. A payment orchestration layer routes transactions across multiple acquiring banks through a single integration. If one relationship changes, traffic reroutes automatically. Your processing never goes fully dark again.

What to avoid:

- Rushing into another aggregator for short-term convenience

- Applying to one processor at a time and waiting for each decision

- Rebuilding on a single-processor setup that creates the same fragility

The goal isn't just to restore processing, but to restore it on infrastructure that doesn't put you back in the same position again.

The MATCH List Risk (important!)

A Stripe termination can trigger a consequence most merchants never see coming: a listing on the MATCH list (Member Alert to Control High-Risk Merchants).

Maintained by Mastercard, it's a database used by every acquiring bank to screen merchant account applicants. If you're on it, most processors will decline your application without explanation, and you'll often only find out you're listed when you start getting rejected.

A MATCH listing typically stays active for five years.

The reason codes most relevant to Stripe merchants:

- Code 04 – Excessive Chargebacks: chargeback volume exceeds 1% of card transactions in a given month, totalling $5,000 or more

- Code 05 – Excessive Fraud: fraud-to-sales ratio exceeds 8% in a month, or fraudulent transactions exceed $5,000

Not every Stripe closure results in a MATCH listing, as general risk policy terminations don't always qualify. But if you're getting declined across multiple new processor applications without a clear reason, it's worth investigating. Stripe's own MATCH documentation outlines the exact reason codes and what triggers a mandatory listing, and it’s currently the clearest breakdown available.

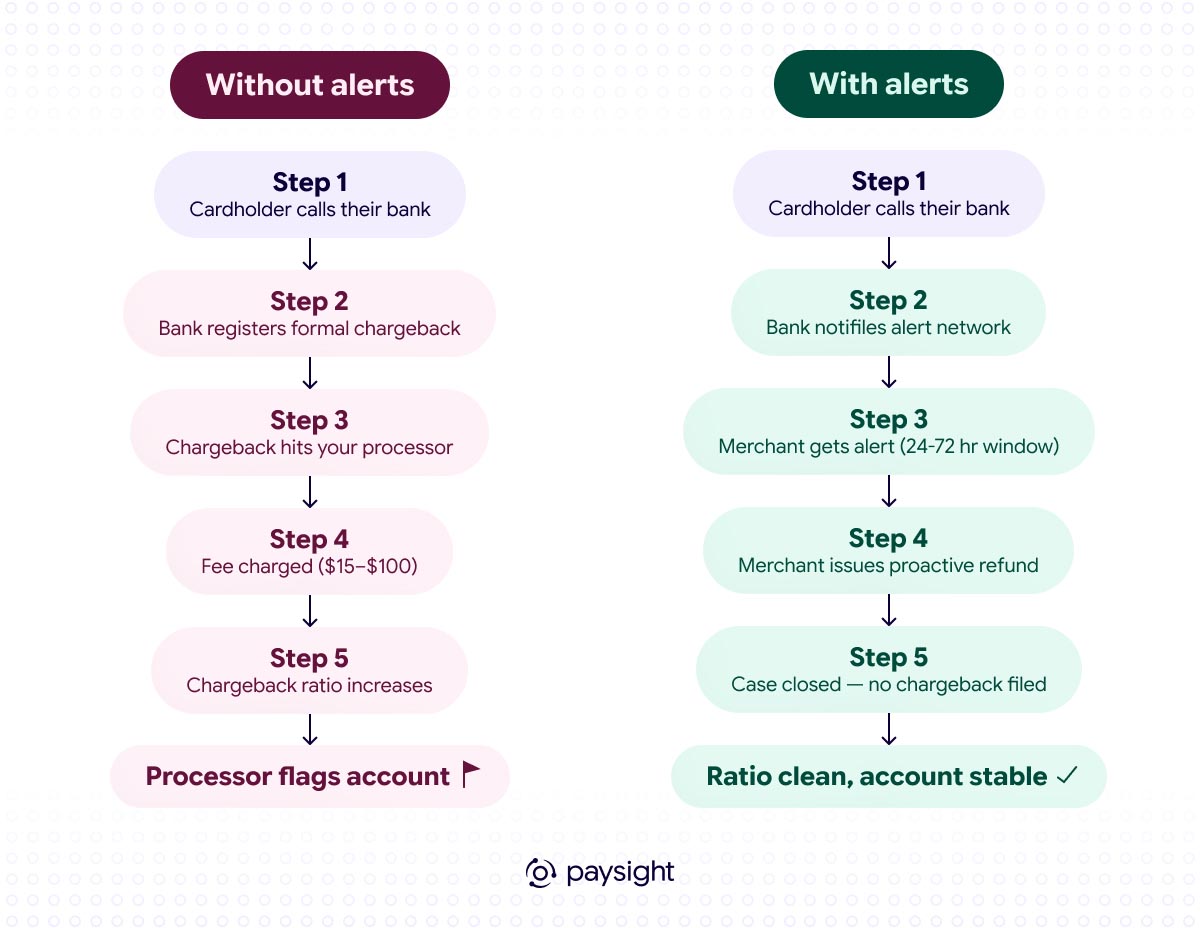

Why Chargebacks Are Usually at the Root of It

In high-risk verticals, elevated dispute rates are often structural, such as subscription charges customers don't recognize, disputes over digital goods, and cross-border billing confusion.

The cost is double: lost revenue plus chargeback fees of $15–$100 per dispute. At scale, it threatens the processing relationship itself.

Chargeback alerts give you a 24–72 hour window between when a cardholder initiates a dispute and when it becomes a formal chargeback. Enough time to refund proactively and keep it off your ratio entirely.

For merchants rebuilding after Stripe, a clean chargeback ratio on the new account is what determines whether the next processor relationship lasts.

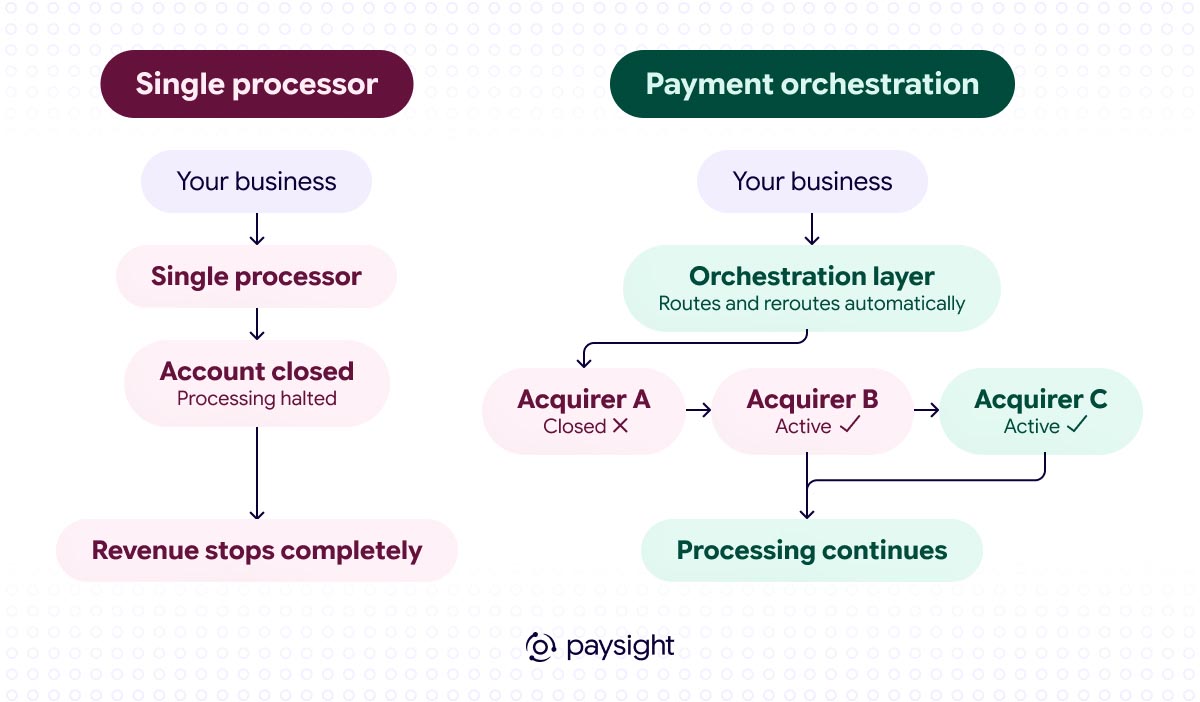

Building Resilient Payment Infrastructure

If Stripe held funds and shut down your account, the worst outcome is rebuilding the exact same single-processor setup and waiting for it to happen again.

The structural fixes are straightforward:

-

Never run on a single processor. One acquirer means one point of failure. Routing across multiple acquiring banks with automatic failover means no single termination halts your revenue.

-

Match your processor to your risk profile. Aggregators serve the mass market. Specialist acquirers underwrite specific sectors. The fit matters more than the rate at signup.

-

Manage chargebacks actively. Real-time alerts, clear billing descriptors, and straightforward cancellation flows keep your dispute ratio in check and your processing relationships intact.

-

Build redundancy into subscriptions. Smart retry logic, dunning sequences, and transparent billing reduce the disputes that put recurring-revenue businesses at disproportionate risk.

The goal is a payment infrastructure that doesn't treat a single processor decision as a business emergency.

How Paysight Supports Merchants After a Stripe Closure

Stripe's shutdown leaves merchants dealing with three distinct problems simultaneously: frozen funds, no payment processing, and uncertainty about what went wrong. Most solutions on the market address one of these in isolation.

Paysight is built around the infrastructure that high-risk merchants need to operate without the fragility that makes a single processor termination a business-threatening event.

- Payment orchestration means your transactions route across multiple acquirers with automatic failover. When one relationship changes, others hold the volume. You maintain processing continuity while you work through the transition. All you need is one integration.

- Subscription management gives recurring-revenue businesses the tooling to handle billing correctly: smart retry logic, dunning flows, clear customer communication, and billing descriptors that reduce confusion. All of this cuts dispute rates before they become a processing problem.

- Chargeback alerts give you the real-time window to intercept disputes before they become formal chargebacks. For merchants rebuilding processing relationships after a closure, keeping the chargeback ratio clean on a new account is non-negotiable. Alert-driven intervention makes that achievable.

If your Stripe account has just been closed, the immediate priority is to stabilize your ability to process. If you want to understand your options, including how to structure processing so this kind of disruption doesn't repeat, talk to Paysight.